Supreme Court silence on $175 billion tariff refund preserves separation of powers

Justices strike down the emergency tariffs but leave the complex, multi-billion-dollar repayment logistics to the statutory framework of the United States Court of International Trade.

The Supreme Court’s refusal to issue a directive on how to return an estimated $175 billion in collected tariffs serves as a deliberate preservation of the separation of powers, not a legal oversight or a defective ruling. Forensic analysis of the court’s decision in Learning Resources, Inc. v. Trump reveals that the justices’ silence operates as a high-stakes guardrail. This intentional omission prevents the judiciary from legislating from the bench and stops the creation of a blueprint for future administrative abuse of the United States Treasury.

President Donald Trump characterizes the decision as a failure because it lacks a single sentence instructing the government on repayment logistics. He labels the ruling deeply disappointing and refers to the justices who vote against the administration as a disgrace. However, providing such a directive requires the court to perform an administrative function that belongs exclusively to the legislative and executive branches under the United States Constitution. Legal experts and forensic trade analysts note that if the court dictates the exact mechanism of a multi-billion-dollar refund, it establishes a rigid precedent that binds all future presidents. Such an action effectively strips the federal government of flexibility in future trade disputes and allows sitting executives to use judicial mandates as a tool to unilaterally manipulate federal funds without congressional oversight.

The executive branch’s vocal frustration over the lack of a refund mandate ignores the permanent nature of judicial directives. By remaining silent on the logistics of the repayment, the Supreme Court ensures that no president can use a court order to circumvent the Anti-Deficiency Act or bypass the congressional power of the purse.

This silence forces the administration and corporate importers to adhere to the established legal mechanics of the United States Court of International Trade. Inside this specialized federal court, individual lawsuits face rigorous vetting to guarantee that only importers who actually pay the tax out of pocket — and do not pass the costs onto American consumers — receive a refund.

Constitutional boundaries limit judicial power

Under Article I, Section 8 of the Constitution, the power to lay and collect taxes, duties, imposts, and excises rests strictly with Congress.

In the ruling, the Supreme Court strikes down the sweeping tariffs because the administration unlawfully repurposes the International Emergency Economic Powers Act to impose taxes.

Chief Justice John Roberts writes in the majority opinion that the statutory authority to regulate importation does not grant the president the independent power to impose tariffs on imports from any country, of any product, at any rate, for any amount of time.

Because the imposition of the tariffs violates the separation of powers, any judicial attempt to orchestrate the refund process commits a similar constitutional violation. The Supreme Court defines the boundaries of presidential power; it does not manage the accounting ledgers of the federal government.

If the justices include a sentence ordering the Treasury to simply return the money, they actively rewrite Title 19 of the United States Code and usurp the legislative branch.

The court’s silence represents a strict adherence to the Major Questions Doctrine, which requires clear congressional authorization for executive actions of vast economic significance. By refusing to write a refund procedure into the ruling, the court maintains a barrier that prevents the executive branch from ever viewing judicial decisions as a blank check for administrative policy.

The forensic reality of the case dictates that the court defines the limits of the law but leaves the administration of that law to the designated federal agencies and specialized courts.

The Trump administration’s impatience with the complex reality of administrative law manifests as a reaction to a standard judicial refusal to overstep.

By not providing a refund blueprint, the justices protect the long-term integrity of the presidency from an executive who might otherwise use a prepackaged judicial remedy to move massive sums of money without the individual vetting required by law.

Customs law dictates strict refund procedures

The statutory framework of 19 U.S.C. 1514 demonstrates exactly why a one-sentence Supreme Court directive for a $175 billion tariff refund remains legally impossible. This federal statute, which governs United States Customs and Border Protection protest procedures, requires a strict, individualized administrative process that no judicial ruling can legally bypass.

Under the law, the assessment of duties becomes final and conclusive upon all persons unless an importer files a formal protest within 180 days of the entry’s liquidation.

Liquidation serves as the final computation of duties accruing on a specific shipment.

The Supreme Court holds no authority to waive this congressionally mandated timeline or the liquidation process itself.

Instead, importers must assess the liquidation status of affected entries immediately.

For unliquidated entries, companies file post-summary corrections. For entries liquidated within the past 180 days, timely protests under 19 U.S.C. 1514 remain critical to preserve refund rights.

Entries liquidated beyond the protest window present complex litigation questions that require direct action in the Court of International Trade.

The forensic reality of customs law requires importers to prove their specific financial injury.

Administrative courts require companies to submit detailed documentation proving they actually pay the tariffs out of pocket and do not pass the costs onto American consumers through higher retail prices.

This legal standard prevents unjust enrichment, ensuring corporations do not receive a massive taxpayer-funded windfall for expenses they already recoup at the cash register.

A blanket judicial refund order from the Supreme Court ignores this evidentiary requirement entirely.

The executive branch’s demand for immediate, sweeping repayment thus conflicts directly with federal law. The text of 19 U.S.C. 1514 establishes that the United States Court of International Trade possesses exclusive jurisdiction to hear these protests only after importers exhaust all administrative remedies.

The Supreme Court’s silence simply enforces the existing statute. The justices force the administration and the importers to follow the exact legal procedures Congress enacts for recovering contested funds, proving that the court prioritizes statutory law over executive convenience.

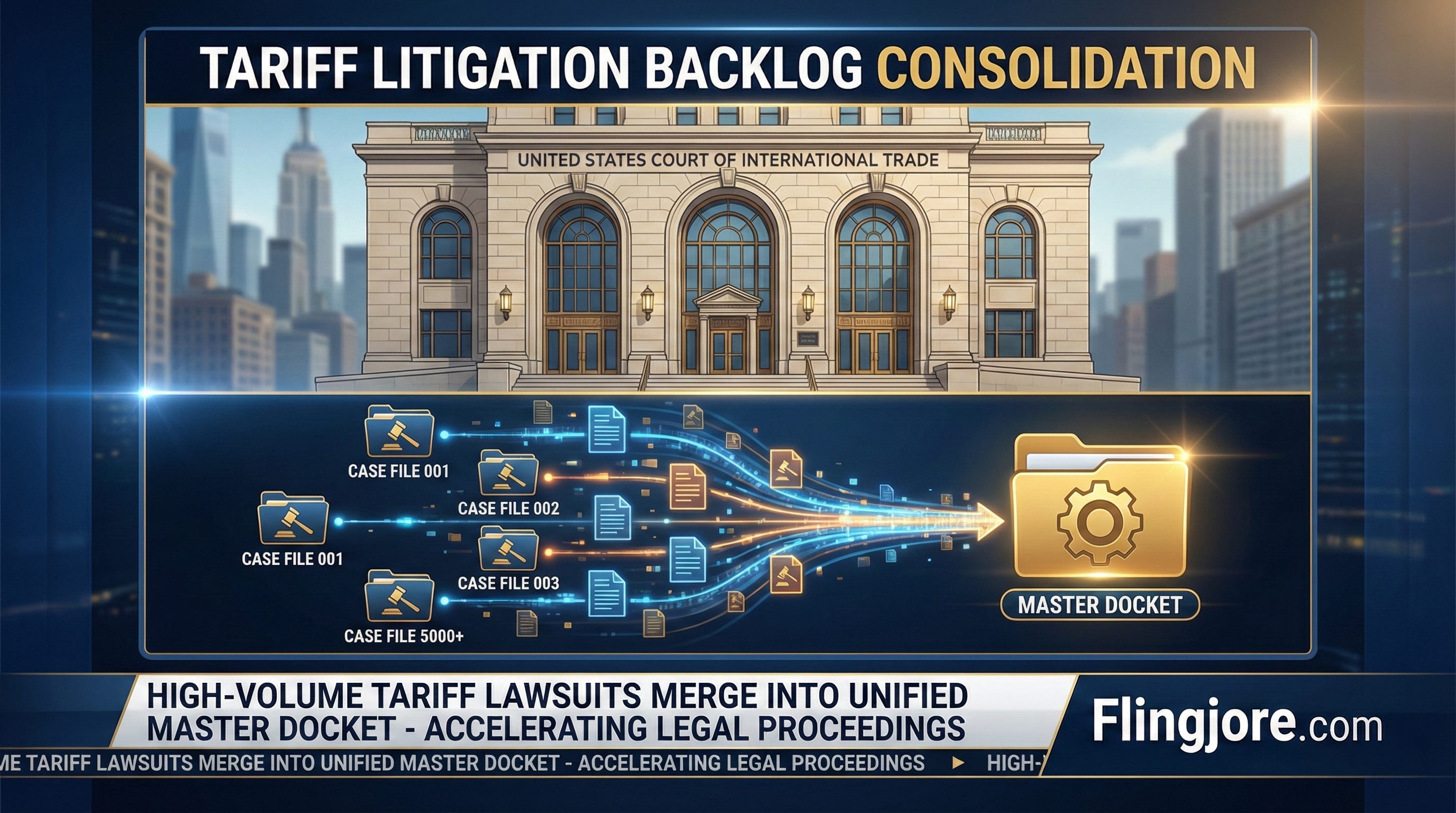

Trade court manages massive master docket

The United States Court of International Trade faces a monumental administrative hurdle as more than 1,500 lawsuits flood its docket in the wake of the Supreme Court decision.

To manage the massive backlog of claims seeking a share of the $175 billion in collected duties, the New York-based trade court relies on a master docket system. This procedural maneuver prevents total judicial gridlock and ensures consistent application of customs law across thousands of individual claims.

Under this framework, a three-judge panel consolidates the thousands of individual corporate lawsuits into a single administrative vehicle.

The judges then designate a test case to litigate the core procedural disputes. In this test case, attorneys for the designated corporate plaintiffs and the Department of Justice argue the specific mechanics of duty recovery.

They debate whether importers properly exhaust their administrative remedies under federal statutes, whether Customs and Border Protection illegally denies corrections for unliquidated entries, and what level of forensic proof companies must provide to demonstrate they actually absorb the tariff costs.

Once the panel issues a ruling on the test case, that legal precedent automatically applies to the thousands of other lawsuits sitting on the master docket.

This approach prevents the court from holding separate trials over the exact same customs regulations. However, the master docket system guarantees that the refund process stretches across multiple years. Importers who file preemptive lawsuits must petition the court for preliminary injunctions to suspend the liquidation of their entries.

If Customs finalizes a tariff entry while the master case stalls in litigation, the importer risks losing the legal right to recover the funds entirely.

The Court of International Trade requires meticulous forensic accounting from every plaintiff.

Companies leverage automated commercial environment data to identify entries approaching liquidation and take timely action to preserve refund rights. They tie import data to the information residing in their chart of accounts, which directly informs their financial statements.

Such a rigorous judicial reality ensures that the judicial branch does not inadvertently authorize a multi-billion-dollar windfall for corporations that fail to follow strict customs protocols. The master docket systematically grinds through the evidence, proving that the recovery of federal revenue remains bound by statutory procedure.

Executive branch pivots to new tariff authority

Hours after the Supreme Court tariff ruling, Trump pivoted to a new legal authority, confirming that the judicial check on executive power functions as intended.

The president announced he imposes new tariffs under Section 122 of the Trade Act of 1974, which is codified as 19 U.S.C. 2132. Unlike the boundless authority claimed under the International Emergency Economic Powers Act, Section 122 operates as a statutory stopgap designed to address fundamental international payments problems and large balance-of-payments deficits.

It grants the administration the power to impose temporary import surcharges up to 15%, but strictly limits the duration to 150 days unless Congress votes to extend the measure.

This immediate shift provides forensic proof that the Supreme Court’s ruling works.

By striking down the permanent, emergency tariffs, the court forces the executive branch back into a framework that includes a congressional sunset clause. This built-in check ensures that the president is not the only executive making unilateral decisions about international taxation. The swift move to Section 122 demonstrates that the administration recognizes the boundaries drawn by the court, even as it publicly criticizes the lack of a refund mandate.

The requirement for companies to file formal protests and endure the master docket system ensures the recovery of these funds remains a matter of verified law rather than executive fiat. The court’s silence acts as a definitive check on power. It ensures the current administration, and all subsequent administrations, cannot abuse the Treasury through a judicial shortcut that the Constitution never intends to exist.